Internal Control Templates

Internal Control Policy and Procedure Templates

Overview

The internal control policies and procedures templates include an 8 page internal control policy, internal control review procedures, Audit Committee responsibility descriptions, and our spreadsheets with over 1,000 internal controls covering both entity level controls and accounting controls. Use the Copedia Internal Controls to develop an internal control system complete with checklists, questionnaires and evaluation tools covering Assets, A/P, A/R, Cash, Checks, Financial Reporting, Job Costing, Marketing/Customers, Data Integrity, Payroll and HR, Project Management, Purchasing, Receiving and Warehousing, Safety, Sales and Estimating, Retail, the Control Environment, Control Activities, Risk Assessment, Information and Communications, and Control Monitoring.

The internal control manual templates are included in the Accounting and Management Template Library or licensed separately.

Internal Control Assessment Tools

The internal control templates are delivered in both text and spreadsheet formats, so you can easily develop and print internal control checklists and questionnaires. You can also use the spreadsheets to evaluate compliance with your internal control system for reporting to governing authorities.

Internal Control over Financial Reporting - ICFR

The Copedia Internal Control over Financial Reporting templates focus on the accuracy and reliability of financial reporting and compliance with GAAP.

Internal Control for Nonprofits

Our internal controls for nonprofit organizations include templates for grants covering allowable costs, program income, property and equipment acquisition, matching, procurement, reporting, contributions, donations, and funds availability. Also included in our nonprofit internal controls are detailed donation collection and cash handling procedures for events and churches

Internal Control Policy and Procedures Manual Template

Contains a 100+ Page Internal Control Manual

Internal Control Policy Template

All Templates download in MS Word and Excel for easy customization.

Includes an 8 Page Internal Control Policy

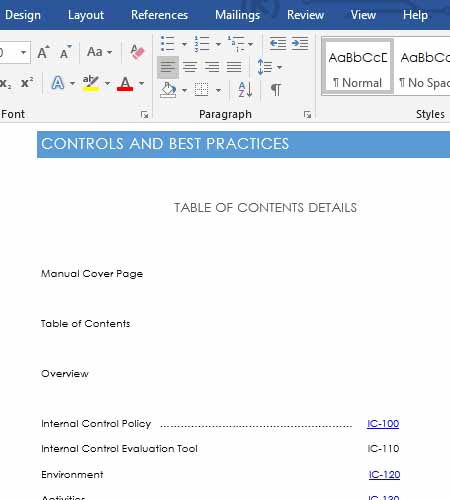

Example Internal Controls

Following are examples from the Copedia internal controls module. First, a screen shot from the Internal Control Assessment Spreadsheet and second, an example checklist of Asset controls in text format:

Templates Download in Word and Excel

All Internal Control Templates download in MS Word and Excel for easy customization.

Internal Control Template

Following is sample internal checklist templateInternal Control of Assets

Division of Duties

___ The person responsible for recording fixed assets does not make general ledger entries

___ The reconciliation of the Fixed Asset detail accounts with the fixed asset control accounts and making entries into the fixed asset software are separate

___ The custodian of the fixed assets and the taking of physical inventory are separate

___ The person responsible for tagging fixed assets is not the fixed asset custodian

___ The person responsible for locating missing fixed assets is not the fixed asset custodian

___ Capital asset purchases require authorization

___ Asset disposals require authorization

General Asset Controls___ There are written procedures for purchasing, receiving, recording assets, and inventory management

___ Asset records properly classify and identify the assets

___ Assets are tagged when received

___ Physical asset inventories are actually performed

___ Physical inventories of assets are performed when transition of employee asset custodians occurs

___ Missing assets are logged in a missing asset log

___ Documentation is prepared when assets are received, sold, moved, transferred, damaged, or disposed of

___ Asset reconciliations are actually performed

___ Asset additions are properly valued

___ Asset capitalization includes costs required to place the asset in service including (direct costs, preparation costs, fees, damages, interest, etc.)

___ Assets gains and losses are properly recorded

___ Assets are adequately insured

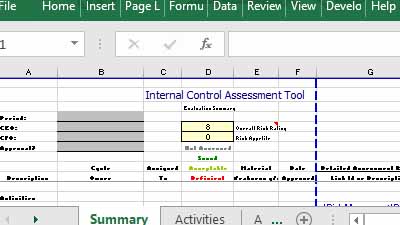

Internal Control Evaluation Tools

Summarize your Internal Control Assessments with the assessment spreadsheet..

Financial and Accounting Controls

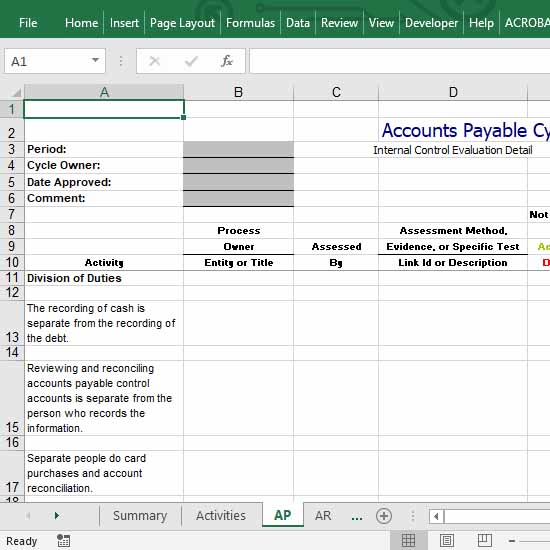

Internal Control - Accounts Payable

A control template covering purchasing, receiving, and accounts payable controls.

Internal Control - Accounts Receivable

A control template covering all AR activities including collections and write-offs.

Internal Control for Nonprofits

Our internal control templates for nonprofit organizations.

Financial and Accounting Control Evaluation Tools

Excel Spreadsheet Tools

Internal Control - Cash

Covers your internal control over cash handling, cash disbursements, and cash receipts.

Internal Control - Payroll and HR

Covers internal controls relating to human resources.

Internal Control - Job Costing

Includes project planning, Purchases, Contract Changes and Modification, Project Costing and Reporting, and Billings. A must have for project related businesses.